eCommerce: Just what the air cargo market ordered

15 July, 2024

By: Tim van Leeuwen

As delegates gathered in Shanghai at the first Air Cargo China conference since 2018, the mood was significantly better than at industry gatherings a year before. Aptly enough the conference was organized in China, the source for the positive mood – with its continued growth of cross-border e-commerce demand.

Quantifying e-commerce volumes remains a challenge. Direct data on e-commerce volumes does not exist, and hence the best indications we have are anecdotal (“more than 50% of our traffic out of Hong Kong is e-commerce”). What information is available on e-commerce volumes, and how do these impact the air cargo market’s near-term outlook?

Air cargo traffic in the lift

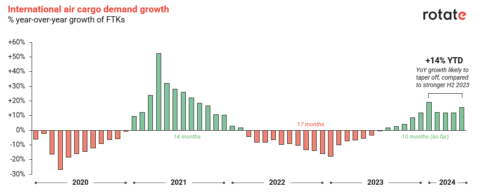

The subdued atmosphere amongst those in air cargo in 2023 was largely due to a slowdown in demand. Air cargo traffic was markedly below the peak volumes of 2021, when pandemic-induced demand significantly boosted volumes. By mid-2023, air cargo traffic had recorded 17 consecutive months of year-over-year declines (see figure 1).

Figure 1: Monthly (year-over-year) growth of international air cargo traffic, as reported by IATA.

Thankfully, fortunes changed in 2023. As of May 2024, air cargo demand is on a run of ten consecutive months of year-over-year traffic growth. The last 6 months even registered double-digit growth. This strong demand is likely to continue in the second half of the year, although the growth will slow to single digits when comparing to a stronger second half of 2023.

Capacity as an indicator for air cargo traffic

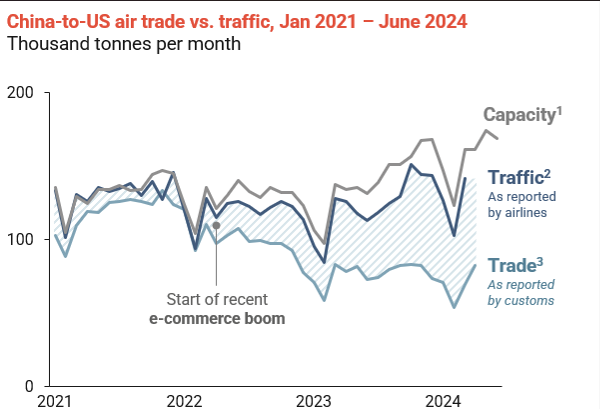

To our surprise, one data source paints a bit of a gloomy picture: air trade data (as reported by customs) has declined in 2024. US customs data shows air trade down 9% on the Transpacific (see figure 2). This contrasts sharply to 21% growth as reported by airline traffic (the dark blue line in figure 2).

The difference in trends between these sources is caused by so-called “de minimis” thresholds of customs authorities, the maximum shipment value allowed to be imported duty-free. As an example, imports into the US are only subject to duty (and hence detailed registration at customs) if their value is over 800 USD. With e-commerce shipments nearly always below this value, customs-based trade data usually does not cover e-commerce volumes, whereas traffic statistics do. With e-commerce demand continuing to grow, the gap between these indicators has swelled significantly since 2022 (see figure 2).

Figure 2: Monthly figures for air cargo trade (as reported by US customs), air cargo traffic (as reported by airlines) and air cargo capacity (from Rotate Live Capacity) between China (including Hong Kong) and the USA. Sources: US Census, BTS, Rotate Live Capacity

Whilst air cargo traffic data gives a better picture of true demand, one disadvantage is that it usually has a significant lag (up to three months). This means it is hard to adjust strategy in real time based of this information. Rotate’s consulting team has found that on high-demand trade lanes (like the Transpacific), real-time air cargo capacity is amongst the best indicators of air cargo traffic (see figure 2). Capacity data is increasingly the best indicator of air cargo demand – especially on lanes highly impacted by eCommerce.

Freighter shortages improve the near-term outlook

With e-commerce volumes representing a sizeable share of air cargo demand out of Asia, delegates at Air Cargo China expressed worries that the air cargo industry is becoming reliant on cross-border e-commerce volumes. A commonly asked question at the conference was around the outlook of the air cargo market for the remainder of the year. Rotate’s consulting team is keeping an eye on three trends in particular.

The first is any potential changes to de minimis thresholds, in particular in the USA where adjustments are being discussed. Given the low-value nature of the shipments though, the threshold would have to be lowered significantly to affect a sizeable number of e-commerce shipments. For now, our capacity data shows no signs of flights into the USA slowing down.

Second is any indications of slowing consumer interest in e-commerce platforms; at Rotate we monitor downloads and usage statistics of popular shopping apps. Again, our analysis has shown consumer interest is unrelenting.

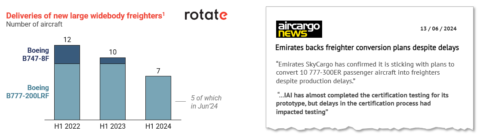

A third trend concerns the supply side, with several forwarders and carriers commenting on the difficulty of obtaining capacity on today’s market. In part this can be attributed to reductions in deliveries of large widebody freighters into the market. As an example, engine supply issues and quality assurance efforts have limited Boeing’s deliveries of B777-200LRF freighters to just 7 so far this year (see figure 3). Ongoing production issues at Boeing (and high demand for passenger aircraft) have also delayed the certification of the imminent Boeing 777-P2F conversion programs.

Figure 3: Slowdown of large widebody freighter deliveries in 2024 (Source: Boeing) and recent news on delays to large freighter conversion programs

All these trends combined mean there is ample reason to believe that the air cargo market will remain strong in the second half of 2024. E-commerce demand will likely continue to play a key role, both in established markets and increasingly in emerging markets. Air cargo continues to deliver on consumers’ unrelenting demand.

Tim van Leeuwen is a strategy consulting project manager at Netherlands-based Rotate, the go-to team in the cargo industry for commercial decision-making.

Want to know more about Rotate, please feel free reach out to us via: commercial@letsrotate.com

About Rotate:

Rotate is helping the air cargo industry to make better commercial and strategic decisions. The company provides software products, market data, and strategy consulting to help the air cargo industry turn data into action. Rotate brings together a unique mix of air cargo experts, strategy consultants, and technology professionals to create real and practical solutions and strategies. The company targets all domains that drive the commercial performance of airlines: from sales optimization and dynamic pricing to revenue management, contract management and revenue leakage.

For press or media enquiries, please reach out to Jonathan Mellink, Head of Sales and Marketing: jonathan@letsrotate.com